!

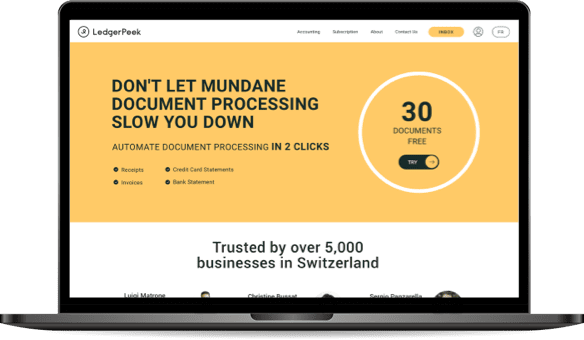

Automate document processing in 2 clicks

To get started in the InBox, open the desktop version

Aplication coming soon

✕

Service Request

Your message has been

successfully sent!

We will get back to you within 24 hours.

OK

Oops! Something went wrong while submitting the form.

Accounting

Subscription

About

Contact Us

Inbox

Inbox

EN▸

English

Français

Italiano

Polski

Deutsch

EN

EN

FR

DE

IT

PL

info@ledgerpeek.com

Oops...

Looks like this page doesn’t exist,

but don’t let that stop you

GO HOME